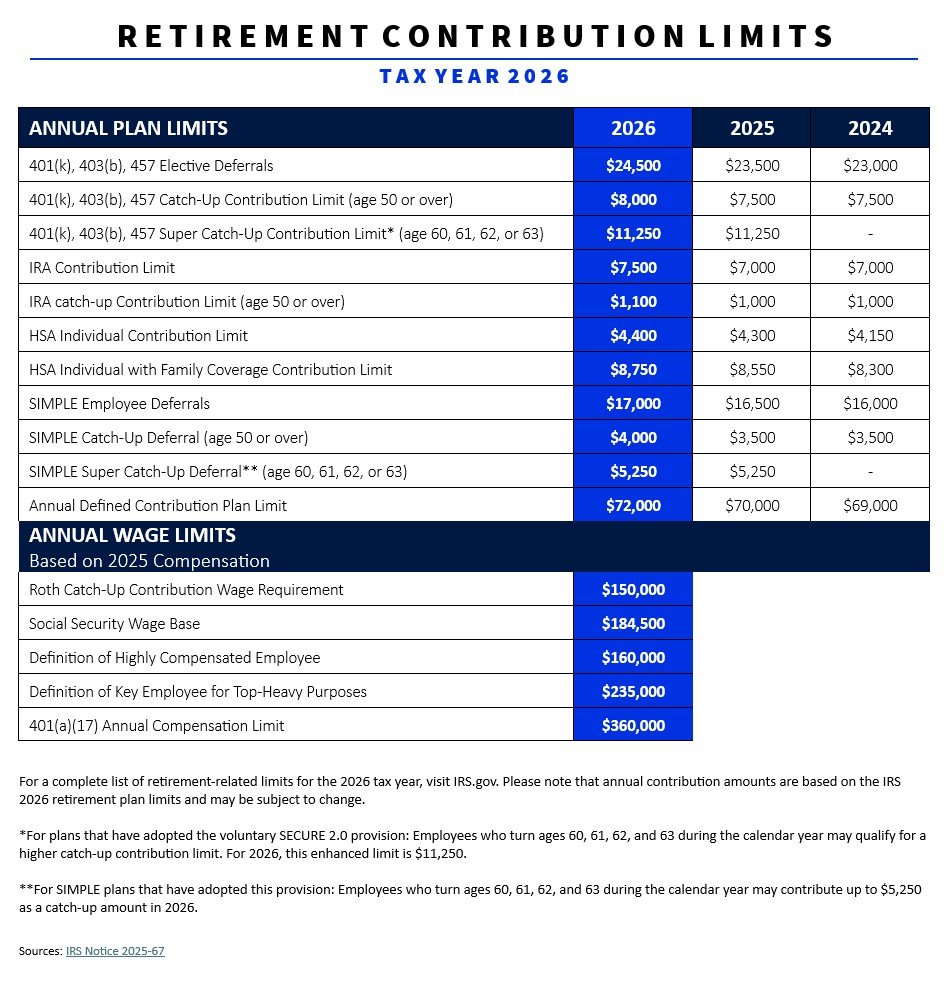

Contribution Limits

Each year, the IRS reviews the annual contribution limits. Increases don't happen every year, so be sure you know your limits.

Annual Contribution Limits on Retirement Benefits and Compensation

Whether you’re an employer who wants to help your employees work toward a secure retirement, or someone who wants to plan for your own future, this guide can help you narrow the focus and zero in on a retirement plan that could work for you in 2026.

For full details on the pension plan limits for 2026, visit the IRS website.

For full details on the pension plan limits for 2026, visit the IRS website.Blog

Tampa, FL AssuredPartners Investment Advisors (“APIA”) is excited to announce the addition of Chesme Capital Management. Based out of Michigan, Chesme Capital Management has been a leading provider...

Tampa, FL - AssuredPartners Investment Advisors (“APIA”) is excited to announce the addition of FSM Wealth. Led by Brian D. Heckert, CLU, ChFC, AIF®, QPFC, FSM Wealth started serving their community...

Tampa, FL - AssuredPartners Investment Advisors (“APIA”) is excited to announce that Susan Sanchez, CPFA, ARPC, AIF®, has joined APIA. Susan is a seasoned financial professional driven by values of...